November 28 2023

1 Min Read

Young companies with groundbreaking business ideas seem like a no-brainer for investors hoping for a big payoff. But the reality is much harsher. For every story about a “VC Unicorn” whose value surpasses a billion dollars, there are countless ventures that fail outright or fall well short of investors' expectations. So why bother with such risky investments? Why exactly do people find Venture Capital so attractive? Let’s explore.

Start-ups typically approach Venture Capital firms with an audacious idea for a company that requires funding to get its business off the ground and to support its rapid growth. The vast majority of these VC-backed companies are technology focused, but healthcare and consumer-focused companies are also key verticals.

Venture Capitalists are focused on finding companies with a specific niche or focus, with a large Total Addressable Market, and a superior management team that provides the best prospects for growth and potential return on capital. Over time, exceptional VC-backed companies have gone public and led to outsized returns, such as Facebook/Meta.

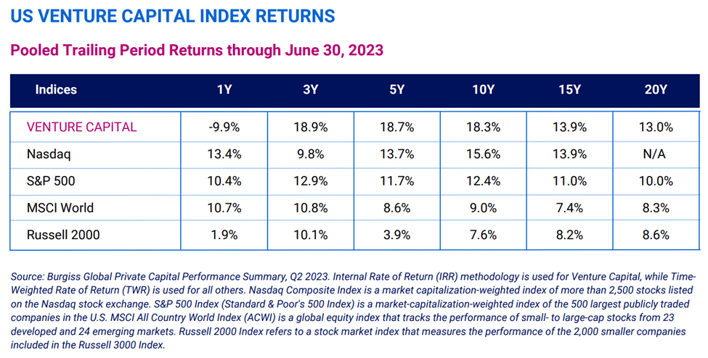

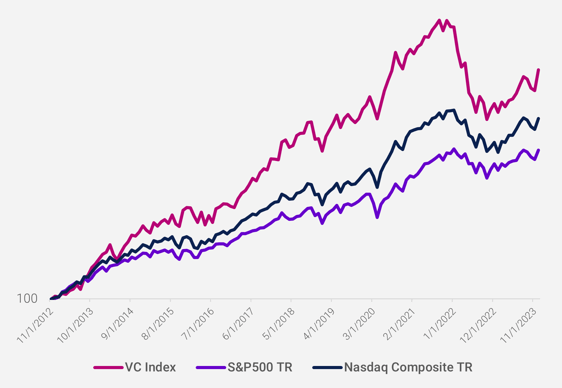

Under the right circumstances, VC managers have been able to deliver attractive returns beyond other equity class investments. Just look at historical returns, which of course are not indicative of future performance.

The Venture Capital universe comprises a huge number of companies in a variety of stages of their lifecycles. With no central marketplace nor universal means to value each enterprise regularly, quantifying the overall performance of the industry is a challenge. One measuring tool is the FTSE DSC Venture Capital Index, which goes by the ticker TRVCI (originally known as Thomson Reuters Venture Capital Index). This index was designed to track the aggregate performance of U.S. companies backed by Venture Capital.

TRVCI was developed in 2012 by research firm DSC Quantitative Group. It is comprised of approximately 150 publicly listed securities optimized to replicate the risk/return profile of the VC industry using extensive Thomson Reuters data (now owned by the London Stock Exchange under the FTSE moniker) that captures the valuations of venture capital-backed companies.

While you cannot invest directly in this index, AXS Investments manages the AXS FTSE Venture Capital Return Tracker Fund (ticker LDVIX), a mutual fund that seeks to provide investment results that correspond generally to the price performance of the FTSE VC Index.

Comparing performance over the 11-year period ending December 2023, VC generated an annualized return of 21.59% (787.45% cumulative), while the S&P 500 returned 13.68% (318.55%) and the Nasdaq grew by 16.81% (467.14%).

Source: DSC Quantitative. VC Index is the TRVCI. Return data is represented logarithmically to account for compounding. Past performance is not a guarantee of future results.

While it’s not possible to predict when the IPO market will normalize and return to a healthy level of new companies going public, we recognize the market moves in cycles. What we can likely anticipate with greater certainty is that the Venture Capital industry will continue to identify and support young, upstart businesses with significant new technologies and ambitious business ideas that will disrupt incumbents and innovate in ways that will change the landscape of commerce. The necessary inputs for these business – daring and bold entrepreneurs, available capital sources, and investors focused on identifying and nurturing these firms – are still in place and constantly on the lookout for the next breakout technology, disruptive business idea, and management team to guide them.

This information is educational in nature and does not constitute investment advice. These views are subject to change at any time based on market and other conditions and no forecasts can be guaranteed. These views may not be relied upon as investment advice or as an indication of any investment or trading intent. This content should not be construed as an offer to sell, a solicitation of an offer to buy, or a recommendation for any security by AXS Investments or any third-party. All investing is subject to risk, including the possible loss of the money you invest.

IMPORTANT RISK DISCLOSURE

Mutual funds involve risk including possible loss of principal. There is no assurance that the Fund will achieve its investment objective. Diversification does not ensure profits or prevent losses.

Mutual funds involve risks including the possible loss of principal. The Fund may invest in ETFs, ETNs and mutual funds, which are subject to investment advisory and other expenses, which will be indirectly paid by the Fund. ETFs, ETNs and mutual funds are subject to issuer, fixed income and risks specific to the Fund. Venture capital investments involve a greater degree of risk; as a result, the Fund’s returns may experience greater volatility than the overall market. The Fund does not invest in venture capital funds nor does it invest directly in the company funded by venture capital funds. The Fund seeks to generate returns that mimic the aggregate returns of U.S. venture capital backed companies as measured by the FTSE DSC Venture Capital Index (TRVCI). There is a risk that Funds’ return many not match or achieve a higher degree of correlation with the return of the TRVCI. Additionally, the TRVCI’s return may not match or achieve a high degree of correlation with the return of the U.S. venture capital-based companies.

Investments in equity securities are subject to overall market risks. To the extent that the Fund’s investments are concentrated in or significantly exposed to a particular sector, the Fund will be susceptible to loss due to adverse occurrences affecting that sector. Loss may result from the Fund’s investments in derivatives. These instruments may be illiquid, difficult to value and leveraged so that small changes may produce disproportionate losses to the Fund. Over the counter derivatives, such as swaps, are also subject to counterparty risk, which is the risk that the other party in the transaction will not fulfill its contractual obligation. In certain circumstances, it may be difficult for the Fund to purchase and sell particular derivative investments within a reasonable time at a fair price.

The AXS FTSE Venture Capital Return Tracker Fund (LDVIX) (the “Fund”) has been developed solely by AXS Investments LLC. The Fund is not in any way connected to or sponsored, endorsed, sold or promoted by the London Stock Exchange Group plc and its group undertakings (collectively, the “LSE Group”). FTSE Russell is a trading name of certain of the LSE Group companies.

All rights in the FTSE DSC Venture Capital Index (the “Index”) vest in the relevant LSE Group company which owns the Index. “FTSE®” “Russell®”, “FTSE Russell®”, “FTSE4Good®”, “ICB®” and “The Yield Book®” are trademarks of the relevant LSE Group company and are used by any other LSE Group company under license.

The Index is calculated by or on behalf of London Stock Exchange Group plc or its affiliate, agent or partner. The LSE Group does not accept any liability whatsoever to any person arising out of (a) the use of, reliance on or any error in the Index or (b) investment in or operation of the Fund. The LSE Group makes no claim, prediction, warranty or representation either as to the results to be obtained from the Fund or the suitability of the Index for the purpose to which it is being put AXS Investments LLC.

Distributed by ALPS Distributors, Inc, which is not affiliated with AXS Investments. AXI000441

Check out our related posts based on your search that you may like